Summary

- Billionaire Charlie Munger recently warned investors.

- He said that commercial real estate is facing severe challenges.

- We discuss the implications for REITs.

- We’re currently running a sale for our private investing group, High Yield Landlord, where members get access to portfolios, market alerts, real-time chat, and more

Recently, I wrote an article entitled “Billionaire Investor Says ‘Buy REITs’” to discuss how Starwood’s CEO, Barry Sternlicht, was pounding the table on REIT investment opportunities. Here is what he said:

“By the way, when credit comes back, you are gonna see REITs take off. REITs are on sale. There are some unbelievable bargains in REITs. We did the same thing during the pandemic. We bought a dozen stocks all over the world and we had a 70% IRR on that stuff. We are already buying some stuff in the public market because I do think that rates are going down.” Barry Sternlicht.

Today, we are going to contrast that with an opposing view.

Billionaire investor Charlie Munger recently said in an interview that he expects a lot of pain in the real estate sector.

In case you are not familiar with Charlie Munger, he is the right-hand man of Warren Buffett. They have both led Berkshire Hathaway Inc. (BRK.B) for decades, and their investment firm has massively outperformed the rest of the market (SP500) under their leadership.

So when he talks, we listen, and he is sending a clear warning to real estate investors:

“A lot of real estate isn’t so good anymore. We have a lot of troubled office buildings, a lot of troubled shopping centers, a lot of troubled other properties. There’s a lot of agony out there.” Charlie Munger.

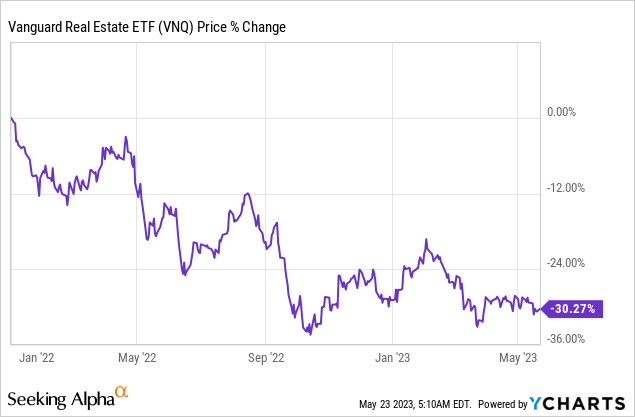

A lot of investors took this as a warning against investing in REITs (VNQ), which are publicly listed real estate investment trusts.

I know this because I have received many messages from investors quoting Charlie Munger as a reason to stay out of REITs.

They are down substantially since the beginning of 2022, and Mr. Munger appears to be warning us of further losses ahead:

But before you panic and run away from all REITs, I want you to take a closer look at what Mr. Munger is saying.

He warned us about two specific property sectors: office buildings and malls.

Then he also said “other properties.” I will assume that he is here referring to single-family homes, which are today unaffordable for most people.

But here’s the thing:

It is only a tiny minority of REITs invest in offices, malls, or single-family homes. Less than 10% of the total market cap of the REIT sector is invested in these properties. So yes, these property sectors may be facing some risks, but they are a small minority.

Charlie Munger appears to be bearish on some of these REITs, and so am I. To give you an example, I sold my position in SL Green (SLG), a NYC-focused office REIT, back in 2021 at a roughly 3x higher share price than that of today.

I have also warned investors about the worrying long-term outlook of outlet centers such as those owned by Tanger Factory Outlet Centers (SKT).

So I agree with Charlie Munger that some property sectors are facing severe challenges.

But what a lot of investors appear to have missed here is that 95% of REITs don’t invest in these challenged sectors. They are mainly invested in strong property sectors that are enjoying high demand and growing rents. Some examples include:

- Warehouses: Prologis, Inc. (PLD)

Prologis

- Distribution centers: EastGroup Properties (EGP).

EastGroup Properties

- Manufacturing facilities: STAG Industrial, Inc. (STAG)

STAG Industrial

- Apartment communities: Essex Property Trust, Inc. (ESS)

Essex Property Trust

- Manufactured Housing: Sun Communities, Inc. (SUI)

Sun Communities

- Data Centers: Digital Realty Trust (DLR).

Digital Realty Trust

(I will skip images because there would be too many…)

- Service-oriented strip centers: Kimco (KIM)

- Net Lease: Realty Income (O)

- Senior housing: Ventas (VTR)

- Skilled Nursing: Omega Healthcare (OHI)

- Hospitals: Medical Properties Trust (MPW)

- Medical Office: Physicians Realty Trust (DOC)

- Self Storage: Public Storage (PSA)

- Timberland: Weyerhaeuser (WY)

- Farmland: Farmland Partners (FPI)

- Billboard: Lamar Advertising (LAMR)

- Cell towers: American Tower (AMT)

- Infrastructure: Uniti Group (UNIT)

- Ground Lease: Safehold (SAFE)

- Etc.

Most of these properties continue to perform very well, and they make up the vast majority of the REIT sector.

Here is a table that I put together to highlight the recent growth of some of these REITs:

| Q1 2023 Same Property NOI Growth | |

| CPT | 8.1% |

| AVB | 10% |

| WELL | 11% |

| SPG | 4% |

| MAC | 4.8% |

| FRT | 3.% |

| REG | 6.3% |

| EGP | 8% |

| STAG | 6% |

You will note that I did not cherry pick REITs from one specific property sector. I included REITs from all sorts of sectors, including residential, healthcare, strip centers, industrial, and even malls.

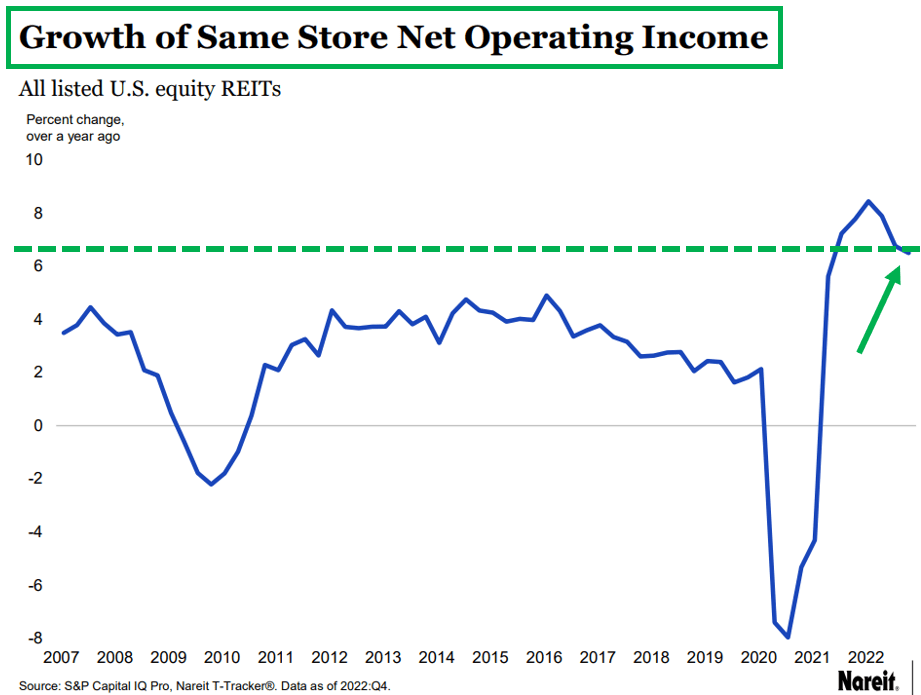

The main takeaway is that rents keep growing at a solid pace across most property sectors, and this is reflected in the chart below. Rents are growing faster than usual because inflation remains high:

NAREIT

But don’t take it just from me. Starwood is one of the biggest landlords in the world, owning $10s of billions worth of properties, and here is what they said recently.

“You have to back up. Other than the office asset class, real estate is actually performing really well. Apartments are full. Single family rentals are full. Hotels are REALLY full. There’s no overbuilding.

What I would like viewers to understand is that the asset class, commercial real estate is actually in very good shape. We are not seeing declines in rents overall in almost anything.

Industrial is strong. Apartments are strong. We have a non-traded REIT and our underlying business is terrific.

What has happened to us is that interest rates have gone up, but if the credit market is right, they will go back down. But the long term effect of rising interest rates is that there is going to be much less supply. So we think that the rent growth will accelerate coming out of this. We will come out of this. We always come out of this. We have never had a recession that didn’t end up with a recovery.” Barry Sternlicht, CEO of Starwood (emphasis added).

So yes, offices and shopping centers may be facing challenges, but they are tiny sub-segments of the REIT market.

The REIT market is vast and versatile and most REITs specialize in strong property sectors that continue to enjoy growing rents.

Here’s the Opportunity

A lot of media headlines keep referring to offices and malls as “commercial real estate,” and it is leading to a lot of confusion.

To give you a few examples:

This recent headline on Seeking Alpha said that Charlie Munger is sounding a warning on the US. commercial property market:

That is not technically wrong, but that is not really what he is doing.

The commercial property market is very vast and versatile, as we explained earlier. It includes 20+ different property sectors, and most are doing just fine.

Mr. Munger is sending a warning about a few specific sub-segments of the commercial property market, not about the entire commercial property market.

Two very different things.

Similarly, CNBC routinely refers to office REITs as “commercial real estate,” seemingly not understanding that offices are just one property sector among many others:

YouTube (CBNC)

(On a quick side note: CNBC apparently also does not realize that Alexandria Real Estate Equities, Inc. (ARE) isn’t an office REIT… It is a life science REIT.)

All of this is causing a lot of confusion, and it has led to the indiscriminate selling of REITs – including even the good ones that are actually performing very well.

Blackstone Inc. (BX), the biggest private equity investment firm in the world talked about this on their most recent Q1 conference call:

“We talked here at the beginning of the call about the massive differentiation across real estate. And now at times you see people just pulling back regardless of the sector they’re exposed to.” John Gray.

Essentially what has happened is that all REITs have crashed as if they were all going through severe difficulties, when in reality, the challenges are mainly affecting one small segment: offices

This has led to a lot of very attractive investment opportunities for long-term-oriented investors because even good REITs are now priced at large discounts relative to the fair value of their properties. Just to give an example: Alexandria, the life science REIT, has been able to hike its rents by 20%+ as its lease expired, but despite that, its share price was cut in half, and it is now priced at a 40% discount to the value of its assets.

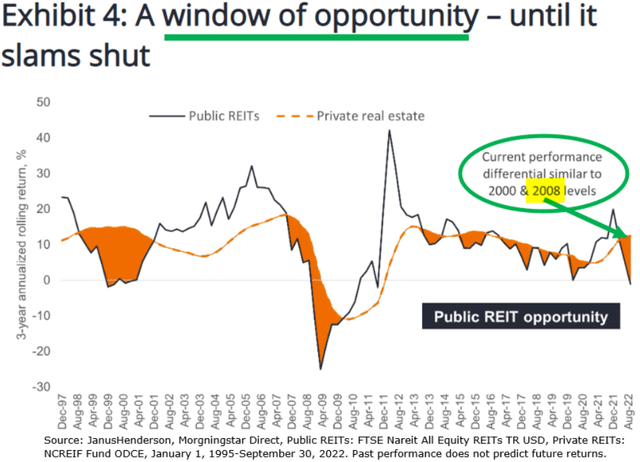

According to some studies, REIT valuations are now reminiscent of the great financial crisis:

Janus Henderson

I believe that this is a great opportunity.

How often do you get the change to buy good real estate at 50 cents on the dollar… with the added benefits of liquidity, diversification, and professional management.

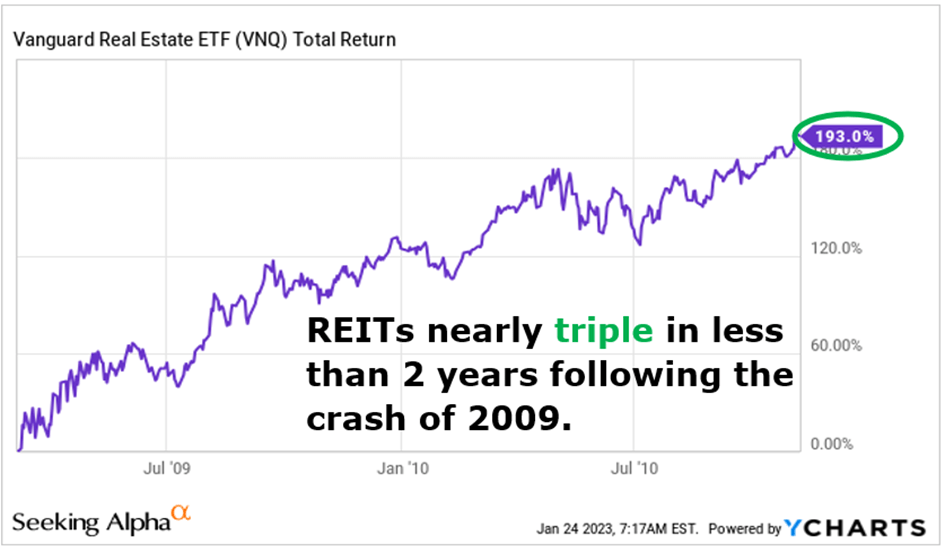

As a reminder, REITs nearly tripled in value in the two years following the great financial crisis as their valuations recovered to more reasonable levels:

YCHARTS

Those who had the courage to buy REITs in 2008 made a fortune in the recovery. I believe that those who buy REITs today will also earn large profits in the coming years.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

SAVE $50 BY SIGNING UP TODAY!

For a Limited-Time – You can join Seeking Alpha’s #1 community of real estate investors at just $29 per month

Try it Free for 2-Weeks. If you don’t like it, we won’t charge you a penny! We have over 500 five-star reviews from happy members who are already profiting from our real estate strategies.

Try it Free for 2-Weeks. If you don’t like it, we won’t charge you a penny! We have over 500 five-star reviews from happy members who are already profiting from our real estate strategies.

We spend 1000s of hours and over $100,000 per year researching the market for the most profitable investment opportunities and share the results with you at a tiny fraction of the cost.

Original Article: https://seekingalpha.com/article/4607070-billionaire-investor-says-sell-real-estate